Scraping the Bottom

The active inventory, buyer demand, and the number of homeowners willing to sell have been bouncing around a bottom all year,

so it is only up from here.

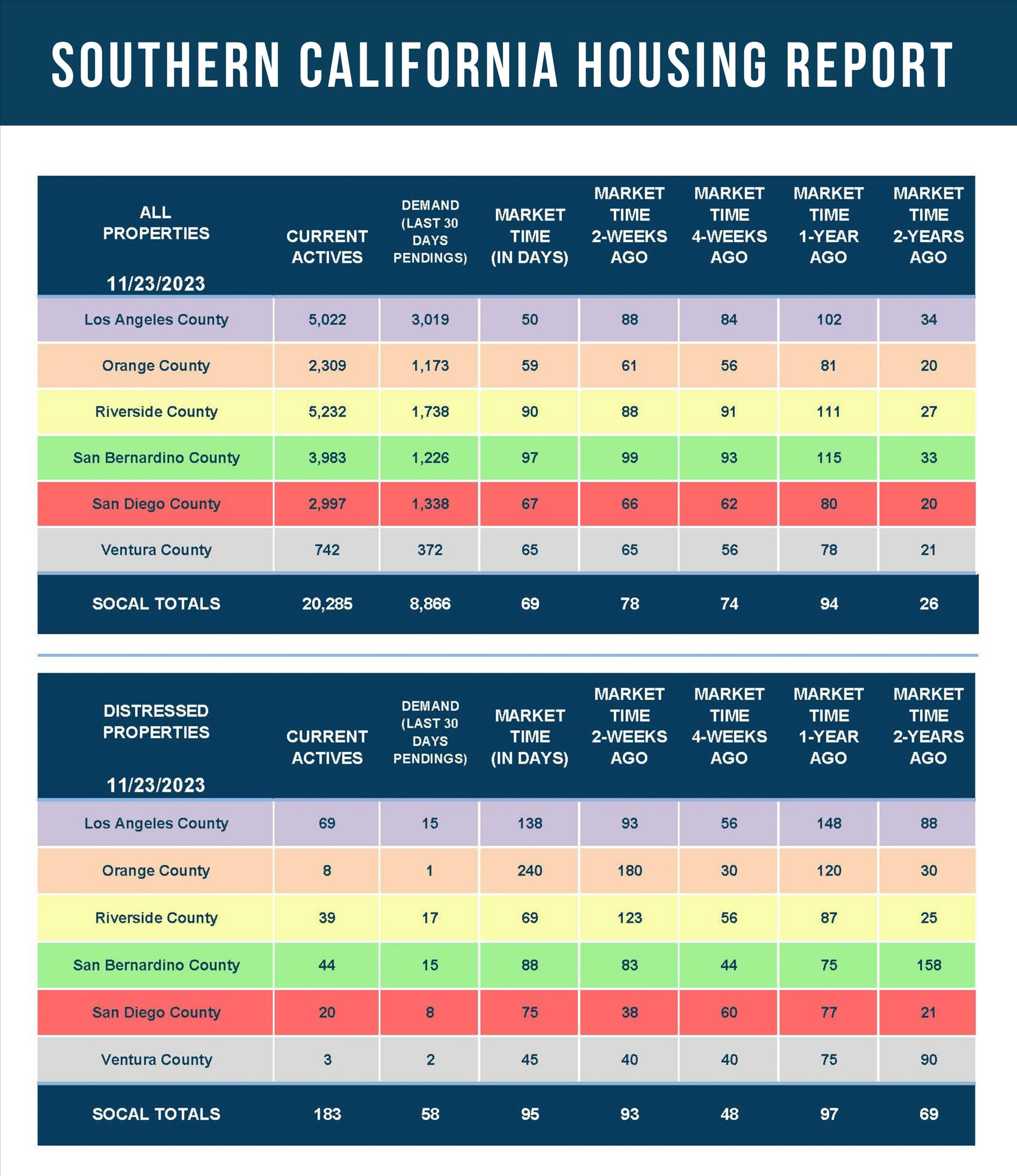

Low Readings for a Year Now

Housing is finally at a point where year-over-year statistics will isolate the slightest signs of improvement in the housing market.

For many, peanut butter is a delectable treat that is wonderful on crackers, toast, bananas, celery and an incredible additional ingredient in chocolate and cookies. The jar often gets to a point where it necessitates scraping the bottom for every last morsel. When it is this low, it is just a matter of time before everything changes; a new jar is opened, and there is plenty of peanut butter to dip into.

Housing is just like that peanut bar jar. The supply of available homes, the number of homeowners willing to sell, and buyer demand are all very low, scraping the bottom compared to normal levels before COVID and sky-high mortgage rates. The current trend lines for these metrics cannot get much lower than where they are today. They have been at these low levels all year. It is just a matter of time before they start to rise from this established bottom.

In October and November, mortgage rates eclipsed 7% for the first time since 2001. They had risen from 3.25% in January 2022 to 7.37% at the end of October, drastically higher in a very short period. The quick erosion in affordability slammed on the brakes of a nuclear-hot housing market.

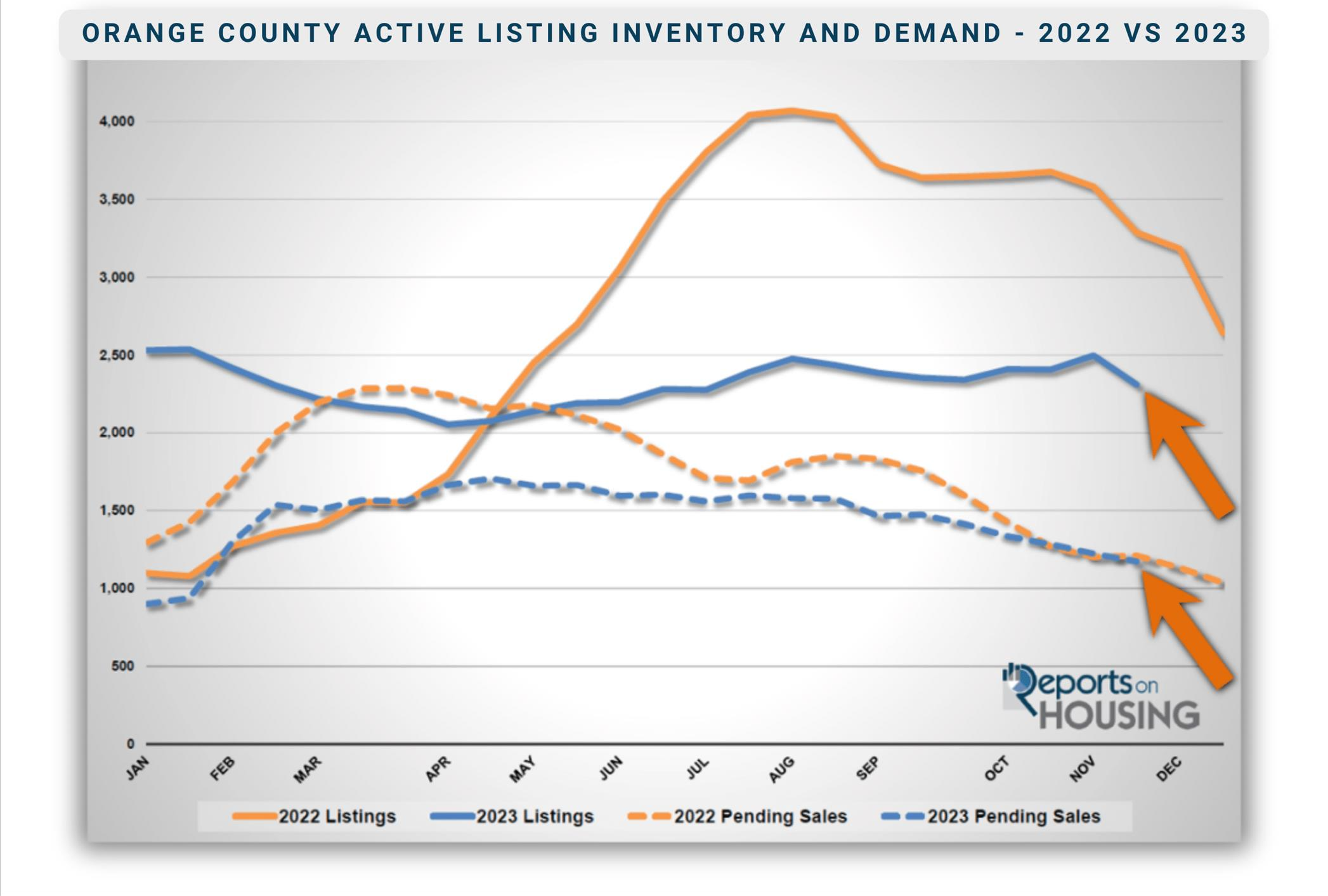

Demand hit a March peak 30% below the average peak for 2020 and 2021. It was 19% below the 3-year average peak in demand before COVID (2017 to 2019). Before homeowners were able to adjust to the much lower demand levels, the inventory climbed from historical lows in January, with only 1,100 homes during the first week, to a peak of 4,069 in August, a 270% rise. It was 60% higher than 2021’s peak at 2,537 homes. Yet, it was still 42% below the 3-year average inventory peak before COVID of 6,959.

Demand in 2023 has been subdued all year due to the high mortgage rate environment and the lack of homeowners willing to sell. Demand has remained relatively flat, at bare-bones, inherent levels. There are always buyers in every market regardless of where rates climb. Year-over-year numbers have been nearly identical for the past month.

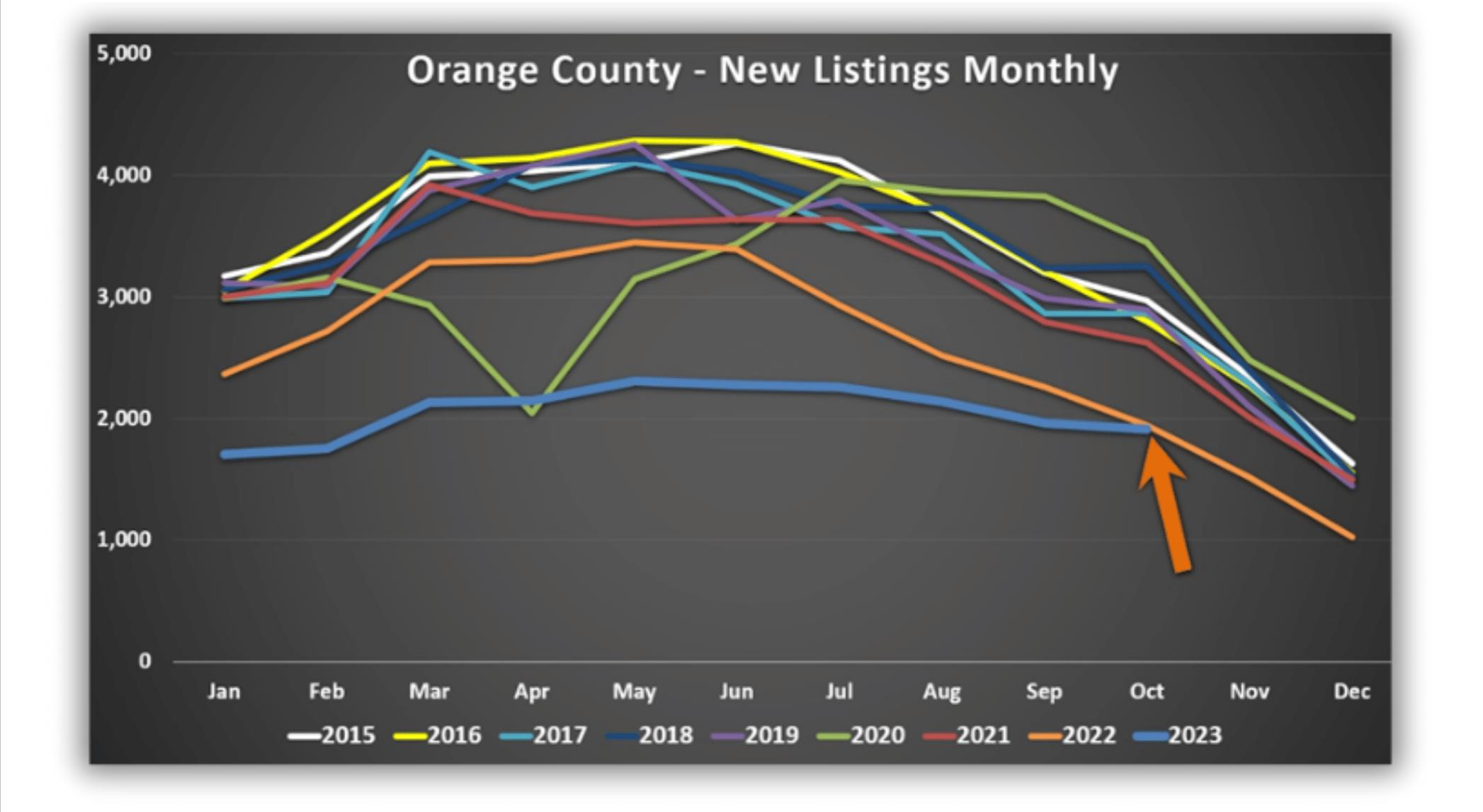

This year’s inventory has also remained relatively flat, dropping by 19% from January through April, when it usually rises. From there, it slowly climbed and did not peak until the beginning of this month at 2,496 homes, 1% below the start of this year. Year over year, there are a lot fewer homes on the market, bare-bones, inherent levels. Like demand, there are always sellers in every market regardless of underlying fundamentals.

Annual comparisons will finally tell a story from this point forward. Housing is scraping the bottom in the number of homes available, buyer demand, and the number of homeowners willing to sell. Any rise in any of these metrics will provide quick insight into the housing market’s direction. The economy is anticipated to cool a bit in 2024 from its hotter pace this year. For investors, a cooler economy typically means a flight to safe, long-term investments, 10-year bonds, and mortgage-backed securities.

This flight to safety results in mortgage rates falling. As rates fall, demand will rise. If rates fall enough, more homeowners will be willing to sell. It is just a matter of time before something finally changes, and there will be more activity in housing. It will not bounce along the bottom forever. A new jar of peanut butter will be opened.

Visit Our Website to Search All Properties

Living or Looking Outside of Southern CA? We have partners everywhere, Let us know how we can help!

CLICK ANY PHOTO TO VIEW CURRENT LISTINGS & CLOSINGS

Real Estate Market Update: Rates Rise, Values Slip

Real Estate Market Update: Rates Rise, Values Slip

Leave a Reply